Many law firm partners struggle to negotiate prices when technology is leveraged as a part of legal services. In a recent Kira-sponsored webinar, Pricing of Technology-Enhanced Legal Services for Today’s Law Firms, Richard Burcher of legal pricing consultancy Validatum provided a road map for thinking about legal pricing when technology is central to the value that firms provide to clients.

One of the most effective pricing strategies, Burcher emphasized in the webinar, is not some complex pricing formula or algorithm. It’s something as simple as a conversation with clients.

Good, Fast, Cheap - Choose Two

The old cliché that customers can have good, fast, or cheap services - but only two of those - governs legal services as well. Lawyers are not good at asking clients to make tradeoffs among alternatives, argues Burcher, but that conversation can be the key to both client and firm walking away satisfied.

Lawyers are not really trained at presenting pricing options, and they are uncomfortable having those conversations, generally preferring to present a more definitive approach to pricing a matter.

That’s an unfortunate attitude, considering that clients are probably in the best position to know what is valuable to them. Is it the fastest and most economical result? Is it the most thorough work, valued because of high risk levels on a matter? Or is time of the essence, due to business or regulatory requirements? Discussing the client’s position on those questions goes a long way to identifying the right mix of technology to be used in a matter, and how to price it most appropriately.

Client Choice as a Negotiation Strategy

Aside from the specifics of different pricing alternatives, simply giving clients a choice among them defuses the situation and puts more control in the client’s hands. The pricing conversation itself becomes part of the trusted advisor relationship that clients say they are looking for in their dealings with law firms.

If a client has alternatives, says Burcher, “the question for clients becomes not whether they are going to use your firm, but which model best captures their risk tolerance on a given deal and the value they place on a positive outcome.” That changes the dynamics dramatically and makes the pricing discussion more of a collaboration and less of an adversarial negotiation process.

The trick is to avoid making assumptions about how a client values different aspects of a matter and what is important to them. The conversation around these things can drive choices about technology, and once those choices are made the firm is in a better position to provide pricing that matches the client’s desired outputs and outcomes, and perceptions of value. In an M&A due diligence context, for example, it’s important to discover whether the customer believes reviewing a select sample of material documents will be sufficient, or whether a comprehensive review of a larger set of documents is required. The answer to that question will drive the alternatives proposed and the pricing for each.

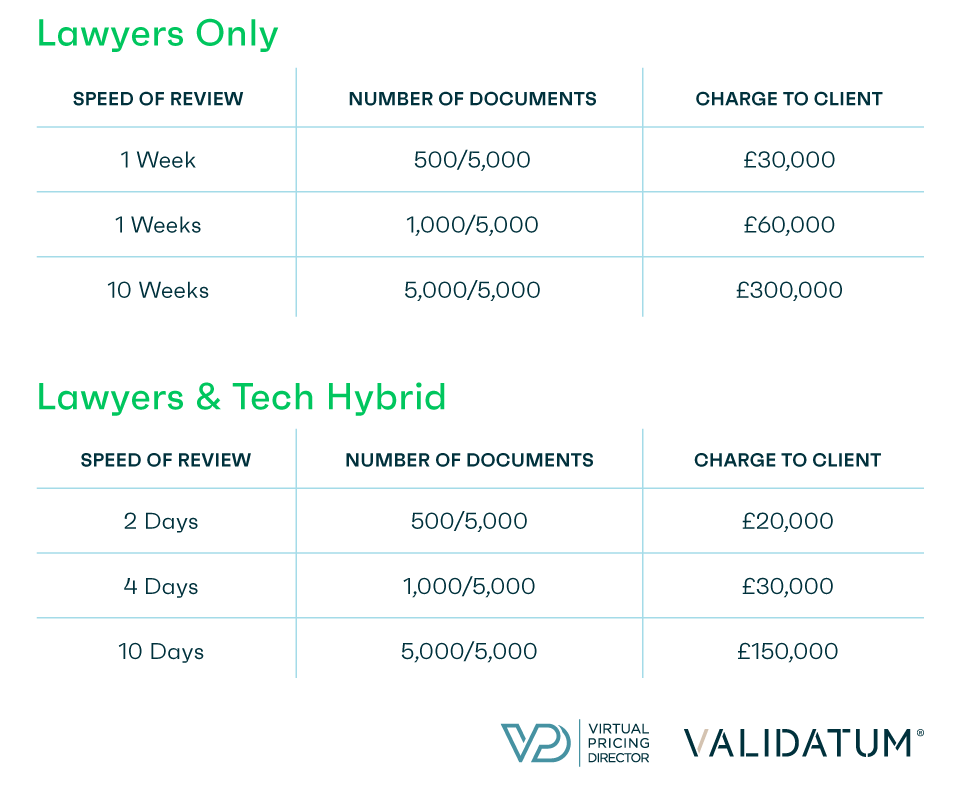

Laying out the various alternatives allows the client to clearly see the alternatives and the prices associated with each, and to choose between priorities - speed, comprehensiveness, and cost. Burcher presented an example from a hypothetical diligence review project, in which it’s clear that the alternatives force the client to match a solution to current needs based on their own requirements rather than the firm’s assumptions.

This approach also allows the firm to adjust the pricing on each alternative to ensure profitability. The option with the most revenue attached to it is not necessarily the most profitable for the firm.

First Steps

First Steps

The webinar concludes with a handful of clear next steps for firms that want to start managing their pricing more strategically:

- Develop pricing models and templates. It shouldn’t be up to the individual lawyer to build pricing models from scratch for each matter “in the heat of battle.” They should be supported by flexible models and templates that allow the firm to price alternatives that are consistent across the firm but appropriate to the specifics of each matter. Pricing directors and legal operations professionals can be very helpful resources here.

- Introduce pricing governance. Consistency of process and approach across the firm is important for efficient pricing processes, and to ensure that best practices are followed.

- Align incentives. As long as billable hours are the primary KPIs for lawyers, it will be difficult to align pricing and value as described above. Partners won’t use effective technologies if their reward systems don’t align with the best outcomes for the firm or the client.

- Teach partners to have the client conversation. The kinds of negotiations and calculations that Burcher discusses here do not come naturally to many lawyers. This aspect of legal practice requires training and practice - the training component is critical.

Burcher believes that there is a short window of opportunity to change the way law firms price their use of technology. It won’t be easy, but the alternative in many cases will be that firms will otherwise wind up giving away the technology they have invested in. Following some of these practices will ensure that clients get good value, and that firms can operate profitably on any technology-intensive work.

A recording of the full webinar is available here: Pricing of Technology-Enhanced Legal Services for Today’s Law Firms.